This article compares the differences between Y Combinator’s pre-money and post-money conversion SAFEs.

TLDR: Our key findings are

- Post-money SAFEs were introduced by Y Combinator in 2018 and started becoming de-facto in 2021. The changes impact Founders and investors in different ways:

- For Founders: Dilution resulting from multiple (and unplanned) post-money conversion SAFES adversely impact Founders.

- For Investors: Be aware of changes to pro-rata and liquidation clauses.

- Most notably, post-money conversion SAFEs transfer dilution risk from investors to Founders. Prior to series A, the post-money SAFE and is generally favorable towards investors.

- Founders’ adverse dilutive impacts come into play in cases of unplanned SAFE financings, for example, a bridge round. As such, Founders can protect themselves by:

- Strengthening budgeting and use of capital planning when raising post-money convertible vehicles.

- More rigorously setting targets and focus on operational fulfillment, particularly on revenue and runway.

- Investors should familiarize themselves with the relevant changes of post-money SAFEs, specifically, pro-rata rights and liquidation preferences.

Introduction

Since Y Combinator introduced post-money SAFEs in 2018, it is quickly becoming the standard for early stage financing in H2 2021. Despite this, the changes are not well understood by both Founders and investors. We set out to demystify these changes in this article.

The following analysis is based on Postmoney SAFE v1.1 and may be found here.

Our comparison of Y Combinator’s latest pre-money and post-money conversion SAFE identified 6 notable changes that impact Founders and/or investors. These changes are detailed below.

The single biggest change and our biggest takeaway is that pre-money conversion SAFEs transfer dilution risk from investors to Founders. Such risk arises when unplanned financing is raised and can be mitigated by Founders through better fundraising strategy and operational execution.

From investors’ point of view, post-money conversion SAFEs shield investors from dilution arising when a portfolio company raises multiple rounds of convertible financing following their investment.

Check out our deep dive into pre- and post-money conversion in these related articles: (pre-money conversion example, post-money conversion example, pre- and post-money side-by-side comparison)

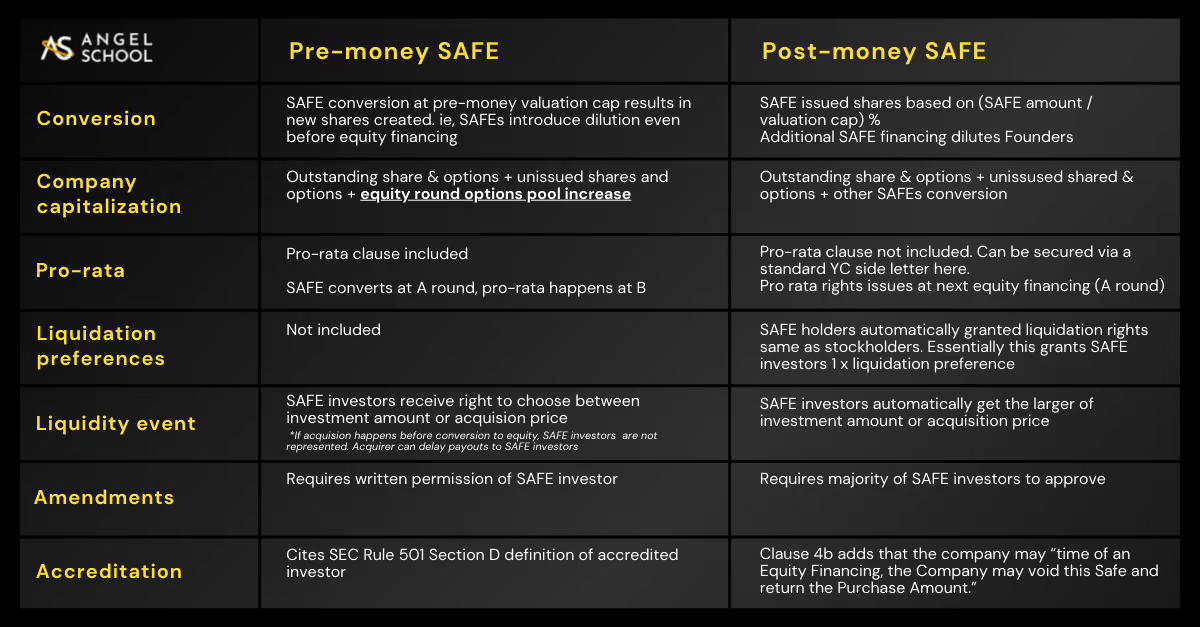

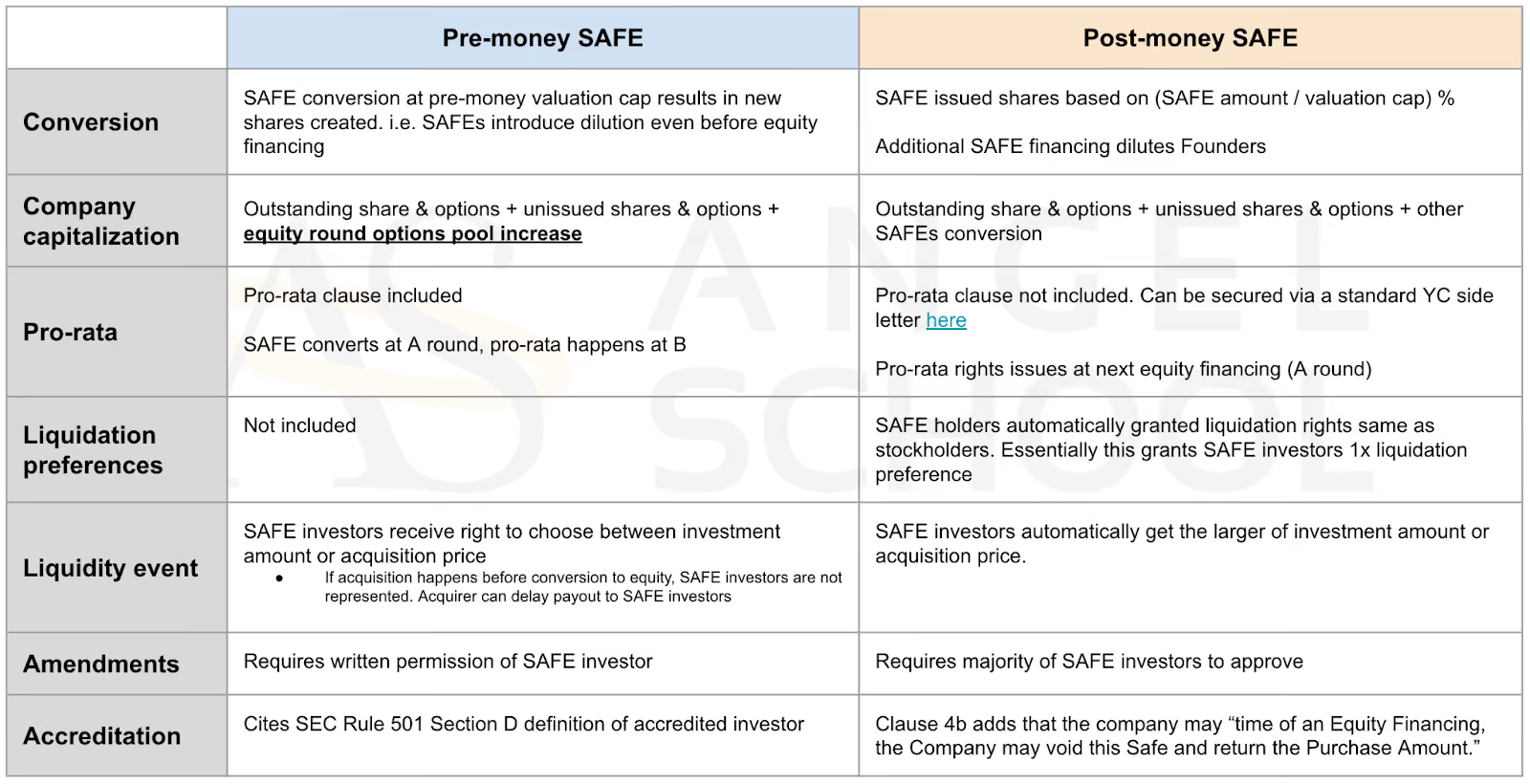

Change #1: Post-Money conversion equity

Theoretically, investing and equity conversion on pre-money or post money bases are identical. A company that is raising $2MN on a $10MN pre-money valuation is the same as $12MN post-money.

The conversion of pre-money and post-money SAFEs into equity during a qualified financing results in new shares being issued based on the valuation cap.

Key changes/ Why it matters:

- Post-money conversion SAFEs simplify cap table math. When converted into equity, post-money SAFEs are issued equity based on (investment $) / (post-money valuation cap).

For example, $2MN raised on a $12MN post-money conversion will see SAFE investors receive $2MN / $12MN = 12.5% of shares. They will subsequently be diluted by the equity investment. - The equity received by post-money SAFE investors is the same regardless of how much non-equity financing is raised and in their form. This is a clear benefit to investors.

The impact is much more profound for Founders. The dilution from every dollar of post-money SAFE capital raised falls entirely on Founders.

Advice to Founders:

Avoiding unplanned future fundraisings to avoid unnecessary early dilution. This can be achieved through:

- Better budgeting, and use of proceeds planning: Plan uses of capital with additional rigor and track its effectiveness on growth.

- Operational execution and target achievement: Model out your business KPIs and execute towards achieving them. This is particularly important when it comes to revenue and runway.

Advice to Investors:

- None. While it is generally beneficial that dilution impact is transferred from investors to Founders, it is a negative signal if your investment is raising multiple rounds of unplanned capital or bridge rounds.

- Longer term, significant Founder dilution can introduce agency problems if Founders shares in the company are too small.

Change #2: Definition of Company Capitalisation

Under post-money conversion SAFEs, company capitalisation is calculated as (i) outstanding shares and options, (ii) unissued shares and options, and (iii) conversion of other SAFEs.

See section 2. Definitions: “Company Capitalisation”

Key changes/ Why it matters:

- Post-money conversion SAFE specifically excludes new options set aside in an equity financing in the definition of company capitalization.

The conversion price per share will be higher under post-money SAFEs compared to pre-money SAFEs. This is because conversion price per share is calculated as (valuation cap) / (company capitalization) AND company capitalization is lower since it omits equity round options pool increases.

Advice to Founders:

- None. Focus on controlling the impacts of unplanned post-money fundraisings outlined in change #1.

Advice to Investors:

- None.

Change #3: Pro-rata rights no longer automatically included

While pro-rata rights were previously included, this is no longer the case with post-money SAFEs. However, investors may verbally negotiate these rights and secure them via a standard Y Combinator side letter (Available here).

Investors are eligible to take their pro-rata at the next round of equity financing.

Key changes/ Why it matters:

- Pro-rata rights are no longer automatically included. Investors will need to discuss and secure agreement with Founders.

- Investors are eligible to exercise pro-rata at the next stage of equity financing with post-money SAFEs.

Under pre-money SAFEs, investors convert to equity and receive pro-rata rights during a qualified equity financing (presumably at series A). They are then eligible to exercise pro-rata at series B.

Early stage investors are more capital constrained than institutional investors. Pro-rata rights are commonly forfeited by Angel investors simply because they cannot afford it. Post-money SAFEs better allow early Angel investors to exercise pro-rata rights since it is ‘cheaper’ to do so at series A than later.

Advice to Founders:

- None.

Advice to Investors:

- Be sure to negotiate for and secure pro-rata rights. It is relatively simple to do so using readily available side letter templates.

- Be aware that you are eligible to exercise your pro-rata at the next equity financing round. Stay up to date on the company’s fundraising timing and plan capital allocation accordingly.

- *Pro tip* Syndicates are a way to fulfill pro-rata rights rather than capitalizing it yourself. Seek out another syndicate lead to partner with or build your own (AngelSchool.vc specifically specializes in helping Angel investors do this.)

Change #4: 1x liquidation preferences included

Under a post-money SAFE regime, investors receive liquidation preferences in accordance with preferred stock, equivalent to receiving 1x liquidation preference. This was not included in pre-money SAFEs.

In other words, post-money SAFE investors will receive their share of proceeds ahead of common shareholders but behind debt.

See section 1. Events, (d) Liquidation Priority

Key changes/ Why it matters:

- Post-money SAFE investors receive protections through preferred shareholder treatment and 1x liquidation preference. This was not the case by default with pre-money SAFEs.

Advice to Founders:

- None.

Advice to Investors:

- Be aware of your liquidation rights.

Change #5: Liquidity event payouts

In a liquidity event, post-money SAFE investors automatically receive the greater of the cash-out amount or the conversion amount set by the valuation cap. On the other hand, pre-money SAFEs give investors a right to choose.

See section 1. Events, (b) Liquidation Event

Key changes/ Why it matters:

- Until SAFEs convert, their investors not equity holders. As such, they do not hold equity rights in a liquidity event. An acquirer can hold on or delay payouts to early SAFE investors. It falls to company management to fight for early investors’ payouts.

This change strengthens SAFE investors’ rights in a liquidity event.

Advice to Founders:

- None.

Advice to Investors:

- None. This is all good news.

Change #6: SAFE amendments ‘dragalong’

Amendments to SAFEs are relatively rare and uncontroversial. One example where amendments are needed post-closing could be in the SAFE discount rate; a conversion based on 20% discount on the next round valuation should be expressed in the SAFE as an 80% discount. This is a common mistake and perfectly legitimate reason for amendment.

Whereas Founders would have to negotiate with each SAFE investor individually and risk having a holdout, post-money SAFEs allow for amendments as long as a majority of investors (based on capital) at that round agree.

See section 5. Miscellaneous, (a)

Key changes/ Why it matters:

- Post-money SAFE amendment ‘dragalong’ streamlines amendments for Founders.

Advice to Founders:

- Be aware of your rights to adjust SAFE terms.

Advice to Investors:

- None.

Change #7: Founders may void SAFEs for accreditation requirements

Adherence to accredited investor requirements are standard for early-stage private investments. The post-money SAFE strengthens this by giving Founders the right to void and return the capital of SAFE investors at the time of an equity financing for failing accreditation.

See section 4. Investor Representations, (b)

Key changes/ Why it matters:

- We do not see this as a substantive change. Founders may exercise this right to remove unqualified investors from their cap table at the time of an equity raise.

Advice to Founders:

- Be aware of your right to remove unqualified investors.

Advice to Investors:

- None

As a follow up, we recommend this 3 article series deep dive into pre- and post-money conversion: (pre-money conversion example, post-money conversion example, pre- and post-money side-by-side comparison)

About AngelSchool.vc

AngelSchool.vc is the ultimate Accelerator for Angel Investors - from 1st check to leading syndicates as ‘Super Angels’. We give venture investors world-class training, a global community AND build their track record as a member of our Investment Committee (IC).

The AngelSchool.vc Syndicate is backed by 1500+ LPs and deploys $MNs annually. Subscribe here for exclusive dealflow.