Funds Managers and Syndicate Leads work to generate an investment profit from investors’ capital and share in this profit by earning carried interest.

We compared carry profitability to GPs using real world data and demonstrate 4.5x higher carried interest payout to syndicate leads over Fund GPs on an average performing

TLDR:

- While there are nuanced dynamics between operating Syndicates and funds, syndicates mathematically generate more profit for their GPs over than VC funds. This is because of how carried interest is calculated on a deal-by-deal basis rather than at the portfolio level.

- We modeled our comparison using 10 years of US VC data from 2009 to 2018. We assumed $5MN of capital deployment, identical portfolio and positions, and carried interest of 20% for both the syndicate and fund. The fund also applies an industry standard hurdle rate of 7% compounded.

The above scenario generates carry of $1.56MN for the syndicate lead whereas fund managers receive $1.31MN. This vastly reduced to $342k when a return hurdle is applied.We therefore conclude that Syndicates have a clear profit benefit over Funds when it comes to GP carry.

Related reading:

- Key Dynamics differences between Funds and Syndicates: A GP Perspective

- Angel School’s Ultimate Glossary of VC Terms

Introduction

Syndicates and VC funds differ on key dynamics in different ways. There are pros and cons to both from the perspective of the Syndicate Lead vs a VC fund GP (for simplicity, we refer to both roles as GPs in this article).

Some differences are intuitive. For example, there is a certain prestige to being a ‘VC backed’ startup. This can offer VCs an advantage in deal access over syndicates. We’ll cover these in a future deep dive on this topic.

One of the clear advantages of syndicates is that they are mathematically more profitable than funds for the GP or Fund Manager. Why is this so? Presuming it is true, how much more profitable are they?The reason is that VC funds calculate carried interest at the portfolio level whereas Syndicates calculate carry on a deal by deal basis; fund investments that produce a <1x return on capital produce a portfolio loss that affects the overall fund profitability. On the other hand, syndicates that return <1x capital result in 0 profit and carry for the syndicate lead. This is even before factoring the hurdle rate on fund carry.

1. The Carried Interest Business Model

The business model of syndicates and VC Funds is based on a model of performance-based profit sharing. This is the concept of ‘carried interest’.

Syndicate leads or Fund GPs make investments into companies in the hopes of exiting those positions for a profit in the future. When a profit is generated, GPs are entitled to a share of profits as defined by the carried interest agreement. The industry standard for carried interest is 20%.

Here’s a simple example:

- An investment is made into a company that is worth $100,000.

- After a few years, the company was acquired for $1,100,000. It has therefore generated a profit of $1,000,000.

- 20% carried interest entitles the GP to $200,000.

- Investors receive $900,000 for an 8x ROI.

2. Syndicates Mathematically More Profitable than Fund

Syndicates and VC Funds calculate carried interest in a slightly different way.

Syndicate carry is calculated on a deal by deal basis. The GP will receive 20% of profit on every single deal that is profitable. Of course, not all investments work out well. Those that do not return <1x on the original investment and can even go to 0. In this case, there is no profit and carry becomes 0.

VC funds calculate carry based on the entire portfolio. In order to earn a single cent of carry, the GP would need to generate a profit on all the investments that exceeds the loss incurred by investments that don’t work out. In this case, losses reduce the portfolio’s profitability which reduces carried interest to the GPs.

Additionally, VC funds typically have return hurdles to compensate LPs for the cost of capital. Hurdle rates are the minimum annual return that the fund needs to generate for LPs before carried interest applies. This is typically around 7% compounded.

3. How Much More Profitable are Syndicates Over Funds

The comparison between Fund and Syndicate dynamics is much more nuanced. We cover this in greater detail in a future article on Fund and Syndicate dynamics from the GP’s perspective. However, the above logic gives syndicates a clear cut mathematical profit advantage over funds.

The question then, is how much more profitable is a syndicate over a fund for their GP? The answer is ‘it depends’. We’ll need to make a number of assumptions to arrive at an answer.

- Assumption 1: The fund and syndicate charges 20% carry. In reality, there is variability in syndicate carry structures.

- Assumption 2: The fund and syndicate invest in an identical portfolio with identical positions. In reality, funds have certain advantages such as being able to deploy capital more quickly.

Assumption 3: No management fees. To normalize the comparison, we assume that the fund and syndicate invest the same amount of capital. Funds typically charge 2% per year of management fee (or 20% of LP capital over a 10 year fund life).

Our Performance Baseline

Portfolio performance affects the outcome. To control this, and to base this analysis in reality, we rely on the below dataset compiled by Seth Levine which shows capital returns for US VC funds from 2009 - 2018. This gives us a proxy of ‘average’ performance.

The histogram shows a long-tail capital return pattern that shows, 51% of capital deployed returns <1x (we take mid-way point and assume 0.5x return. 31% of capital returns 1 - 3x (we assume 2x returns)

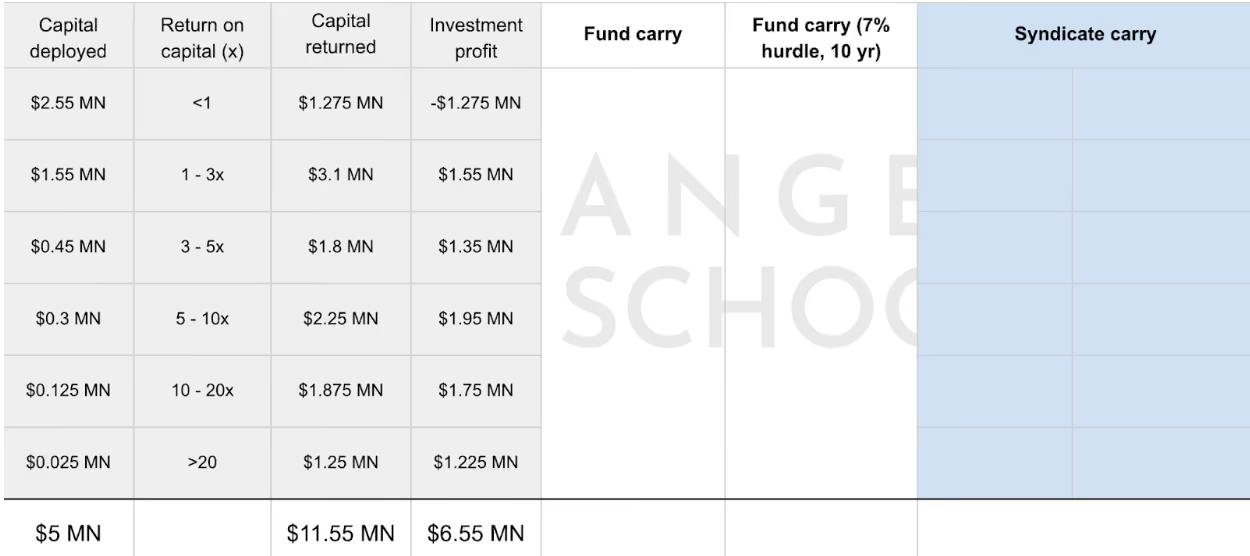

$5MN of Capital Deployment

Assuming the GP deploys $5MN based on this pattern, ~$2.5MN (51% of capital) deployed returns <1x, ~$1.5MN (31% of capital) deployed returns 1 - 3x and so on.

Results of our Analysis

1. Based on the capital return performance data, $5MN of capital returns $11.55MN or $6.55MN profit.

2.GP Carry on the fund model pays out $1.3MN to the GP on 20% carry. However, applying a 7% hurdle rate compounded for 10 years reduces GP carry to a mere $342,860

3. Finally, we look at Syndicate carry. This yields GP carry of $1.56MN. The reason for this difference lies in how loss making investments do not diminish the profit from winning bets.

Conclusion

Based on this example, we can conclude that with an identical portfolio and average performing investments, Syndicate Leads earn 20% higher carry than Fund GPs.

When return hurdles are factored in, the Syndicate generates 450% higher carry ($1.56MN vs $342k) than with a fund.

While there are other dynamics that make the comparison more nuanced, the clear difference in economics makes a compelling argument in favor of syndicates.

Other reading:

- Key Dynamics differences between Funds and Syndicates: A GP Perspective

- Why Emerging Fund Managers should start with a syndicate

About AngelSchool.vc

AngelSchool.vc is the ultimate Accelerator for Angel Investors - from 1st check to leading syndicates as ‘Super Angels’. We give venture investors world-class training, a global community AND build their track record as a member of our Investment Committee (IC).

The AngelSchool.vc Syndicate is backed by 1500+ LPs and deploys $MNs annually. Subscribe here for exclusive dealflow.