Angel investors typically have many questions about participating vs non-participating liquidation preferences.

What are the differences between these two types of preferences? How do they affect calculations and structuring deals? We’ll look at how each type works, understand the calculations associated with them, learn how to structure deals, and discover potential tax implications that come with both types of preferences.

In this blog post, we'll explore all these topics and more as we discuss participating vs non-participating liquidation preference in detail. We’ll look at how each type works, understand the calculations associated with them, learn about ways to structure deals and discover potential tax implications that come along with both types of preferences.

Ready for your next investment? Gain exclusive access to the best companies that Angel School has vetted. Our investors see success through our excellent deal flow and world-class diligence. We source hundreds of companies and invest selectively, with a fully transparent process. The best part? You are 100% in control, and Angel School is 100% with you. Invest only with full conviction. And with our 20% carry, we only profit when you do. That's right--no annual capital commitments. So join our growing global community, and see what a diversified deal flow and a talent for choosing good deals can do for you.

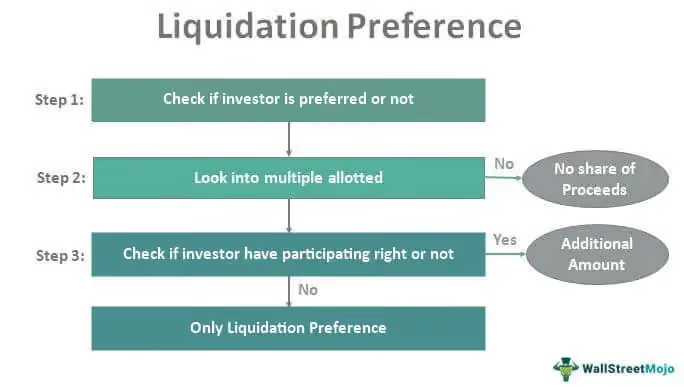

What is Liquidation Preference?

In order to understand participating vs non-participating liquidation preferred stock, let’s understand liquidation preference first. Liquidation preference is a contractual agreement between investors and companies that determines the order in which investors are paid out in the event of a liquidation or sale of the company. It can be used to protect investor interests, as well as provide additional capital for growth.

Liquidation preference gives investors priority over other shareholders when it comes to receiving proceeds from an exit event such as an acquisition or IPO. This means that if there are not enough funds available to pay all shareholders, then the liquidation preference will determine who gets paid first and how much they receive.

Investors typically receive their initial investment plus any accrued interest before other shareholders get anything.

In venture-backed startups, liquidation preference is one of the most negotiated terms in a term sheet. Investors want downside protection in case the startup exits at a lower valuation than expected. At the same time, founders want to ensure that liquidation preferences do not excessively dilute their returns in successful exits. This balance between protection and fairness is exactly why understanding the difference between participating and non participating preference shares is so important for both sides of the table.

The participating liquidation preference meaning refers to a structure where investors not only receive their original investment back but also participate in the remaining distribution as common shareholders. Meanwhile, the non participating liquidation preference meaning refers to a structure where investors must choose between either taking their liquidation preference or converting to common shares to participate in the proceeds. These structural differences significantly influence investor outcomes in different exit scenarios.

Types of Liquidation Preference

There are two main types of liquidation preferences: participating and non-participating.

Participating liquidation preference allows investors to share in any remaining proceeds after their initial investment has been returned, while non-participating liquidation preference does not give them this right. In addition, some investments may have multiple tiers with different levels of protection depending on how much money was invested initially or what type of security was purchased (e.g., participating vs non participating preferred stock).

Advantages and Disadvantages of Liquidation Preference

In venture-backed startups, liquidation preference is one of the most negotiated terms in a term sheet. Investors want downside protection in case the startup exits at a lower valuation than expected. At the same time, founders want to ensure that liquidation preferences do not excessively dilute their returns in successful exits. This balance between protection and fairness is exactly why understanding the difference between participating and non participating preference shares is so important for both sides of the table.

The participating liquidation preference meaning refers to a structure where investors not only receive their original investment back but also participate in the remaining distribution as common shareholders. Meanwhile, the non participating liquidation preference meaning refers to a structure where investors must choose between either taking their liquidation preference or converting to common shares to participate in the proceeds. These structural differences significantly influence investor outcomes in different exit scenarios.

Participating vs Non-Participating Liquidation Preference

There are two types of liquidation preferences: participating and non-participating.

Participating liquidation preference allows investors to receive their initial investment plus a share of any remaining proceeds from the sale or dissolution, while non-participating liquidation preference only allows them to receive their initial investment with no additional proceeds.

The benefit of participating liquidation preference is that it provides more protection for investors since they can get both their original investment back as well as a portion of any remaining proceeds from the sale or dissolution. On the other hand, non-participating liquidation preference offers less protection since it only guarantees that they will get their original investment back without any additional returns.

Ultimately, it comes down to personal preference and what kind of return you expect from your investments over time. It is important to consider the level of risk that you are willing to take on when deciding between participating or non-participating liquidation preference as they both offer different levels of protection and potential returns.

Comparison: Participating vs Non-Participating Liquidation Preference

To clearly understand the participating vs non participating liquidation preference structures, the following table summarizes the key differences between the two. This comparison highlights how investor payouts, risk protection, and exit outcomes differ across the two structures.

Calculations for Participating vs Non-Participating Liquidation Preference

When calculating participating vs non-participating liquidation preferred stock values, you need to know three things:

- Total proceeds available.

- Investor's percentage ownership.

- Investor's pre-money valuation (PMV).

With this information, you can determine what portion of proceeds each investor should expect based on their PMV and ownership percentage as well as whether they qualify for participation rights under the liquidity preference agreement.

For example, let’s say an investor has 10% ownership in a startup valued at $1 million prior to raising funds, with a participating liquidity preference agreement attached. If during exit proceedings there was $10 million available for distribution among all stakeholders involved, then this particular investor would be entitled to 10% x ($1M + $9M), which equals $990,000. This means they would get back both their original investment plus 90% of the remaining proceeds.

How Do These Preferences Affect Investors' Returns?

As an investor, you always want to receive the highest return on your investment. But what happens when there's more than one investor involved in a startup? That's when things like participating vs non-participating liquidation preferred stock come into play.

As the names suggest, participating preference means that the investor will receive their money back first, plus a percentage of any additional proceeds. Non-participating liquidation preference, on the other hand, means that the investor will only receive their original investment back, no matter how much the company is sold for. So, which is better?

If the company is sold for a low price, then non-participating liquidation preference is better because you at least get your money back. But if the company is sold for a high price, then participating preference is better because you get a cut of the profits. It's important to understand the different types of liquidation preferences when you're investing in a startup.

If you want to maximize your return, participating preference is the way to go. However, if you're more risk-averse, non-participating liquidation preference may be a better choice. Ultimately, it's up to you to decide which type of preference is right for you. No matter what you choose, make sure you do your research and understand the risks involved.

How Liquidation Preferences Work in Real Startup Exit Scenarios

Understanding the participating liquidation preference meaning becomes much easier when we look at how these structures work in real exit scenarios. Startup exits rarely follow perfect outcomes. Sometimes companies sell for modest valuations, and sometimes they produce large venture-scale returns. Liquidation preferences determine how those outcomes are distributed between founders and investors.

Scenario 1: Low Exit Outcome

Imagine a startup that raised $2 million from investors at a $10 million valuation. If the company is later sold for $3 million, the liquidation preference clause determines who gets paid first.

If the investors hold a 1x participating liquidation preference, they first receive their $2 million investment back. The remaining $1 million is then distributed based on ownership percentages. This structure ensures that investors recover their capital before common shareholders receive any proceeds.

Under a non participating liquidation preference meaning structure, investors would simply take their $2 million preference payout. Since converting to common shares would provide less than $2 million, the preference payout becomes the better option.

Scenario 2: Moderate Exit Outcome

Now imagine the same startup exits for $15 million. With participating liquidation preference, investors receive their $2 million preference first and then participate in the remaining $13 million based on their ownership percentage. This can significantly increase investor returns in mid-range exit scenarios.

With non-participating liquidation preference, investors must choose between their $2 million preference or converting to equity ownership. If they own 20% of the company, converting would provide $3 million, which becomes the better option.

Scenario 3: High Exit Outcome

In large exits, the difference between participating vs non participating liquidation preference becomes less significant. Investors often convert to common shares because their ownership percentage yields far higher returns than the liquidation preference.

These examples highlight the key difference between participating and non participating preference shares: participating structures favor investors in moderate exits, while non-participating structures create more balanced outcomes between founders and investors.

Tax Implications of Liquidation Preferences

For investors, participating liquidation preferences allow them to receive their initial investment plus a portion of any profits before other shareholders get paid out. This means that they will be taxed at ordinary income rates rather than capital gains rates which can result in higher taxes overall.

On the other hand, non-participating liquidation preference does not provide this benefit as all profits are distributed equally among all shareholders regardless of their original investment amount so it will be subject to capital gains taxes instead.

For companies, participating liquidations mean that they must pay out more money upfront which could potentially limit their growth potential if there isn't enough cash flow available to cover these payments while still meeting other obligations such as payroll or rent costs.

When dealing with a non-participating liquidation preference, companies may find themselves paying out more money than necessary because multiple shareholders each have an equal claim on any profits generated by the company.

Investors should also consider jurisdiction-specific tax regulations when evaluating liquidation preferences. In some countries, the structure of preferred shares can influence how distributions are classified for tax purposes. For example, certain payouts may be treated as dividends, while others may be treated as capital gains. These distinctions can significantly impact the net return on investment.

Because of these complexities, angel investors often consult legal and tax professionals before finalizing investment agreements. Understanding the participating liquidation preference meaning and the non participating liquidation preference meaning within the context of local tax laws ensures that investors make informed decisions and avoid unexpected liabilities during exits.

What Angel Investors Should Look for in Liquidation Preference Terms

For new angel investors, liquidation preference clauses can sometimes look like small technical details in a term sheet. In reality, they are one of the most important economic terms in venture investing. Understanding how to evaluate these clauses can significantly impact long-term investment returns.

1. Preference Multiple

Most venture deals use a 1x liquidation preference, meaning investors receive their original investment back before other shareholders. However, some deals may include 2x or even 3x preferences, which can dramatically change how exit proceeds are distributed. Higher multiples provide stronger investor protection but may reduce founder incentives.

2. Participation Rights

One of the most important questions to ask is whether the preferred shares include participation rights. If they do, investors may benefit from both downside protection and upside participation. Understanding the participating liquidation preference meaning helps investors evaluate whether the structure aligns with their risk-return expectations.

3. Participation Caps

Some deals introduce capped participation to limit how much investors can earn through participation rights. For example, a 3x cap means investors can participate in distributions only until they reach three times their original investment. After that point, remaining proceeds go entirely to common shareholders.

4. Conversion Rights

Conversion rights allow investors to convert their preferred shares into common shares during an exit. This feature is essential in non participating liquidation preference structures because it allows investors to choose the option that produces the highest return.

5. Stack of Investor Preferences

In startups with multiple funding rounds, liquidation preferences can stack on top of each other. This stack determines the order in which investors are paid during an exit. Angel investors should carefully evaluate whether their preference ranks senior, junior, or pari passu with other investors.

By carefully reviewing these terms, angel investors can better understand the difference between participating and non participating preference shares and how those structures affect their potential returns.

Common Mistakes Angel Investors Make With Liquidation Preferences

Liquidation preferences are designed to protect investors, but many angel investors misunderstand how these clauses work in real startup exits. Misinterpreting these terms can lead to incorrect assumptions about potential returns. By understanding the participating liquidation preference meaning and the non participating liquidation preference meaning, investors can avoid common pitfalls that affect portfolio performance.

1. Ignoring liquidation preference in the term sheet

Many new angel investors focus heavily on valuation and ownership percentage while overlooking liquidation preference clauses. However, liquidation preferences often have a bigger impact on actual returns than valuation alone. A high valuation with aggressive participating preferences can sometimes produce worse outcomes than a lower valuation with balanced terms.

2. Misunderstanding participation rights

A common mistake is assuming that participating and non-participating preferences behave the same in exit scenarios. Participating preferences allow investors to receive their preference payout and share in the remaining proceeds, while non-participating preferences require a choice between the preference payout or converting to common shares. Misunderstanding this can lead to overestimating returns.

3. Overlooking stacked liquidation preferences

In startups with multiple funding rounds, each new investor may receive their own liquidation preference. These preferences can stack, meaning later investors may get paid before earlier investors. Angel investors should carefully evaluate where their preference sits in the capital stack to understand actual exit outcomes.

4. Not considering founder incentives

While strong liquidation preferences protect investors, overly aggressive terms can discourage founders and employees. If founders feel that most exit proceeds go to investors, they may be less motivated to pursue moderate acquisitions or grow the company. Balanced structures promote healthier long-term incentives.

5. Assuming liquidation preferences always matter

Some investors assume that liquidation preferences always influence payouts. However, during very large exits, most investors convert preferred shares into common shares because their equity ownership yields higher returns. In such cases, the difference between participating and non-participating preference shares is less significant.

By avoiding these common mistakes, angel investors can better evaluate venture deals and understand how liquidation preferences impact real-world investment outcomes. A solid grasp of participating vs non participating liquidation preference helps investors negotiate smarter terms and build a more resilient startup portfolio.

FAQs About Participating vs Non-Participating Liquidation Preference

1. What are participating and non-participating preference shares?

- Participating: Participating preference stockholders are entitled to both dividend payments and any leftover profit.

- Non-participating: These stockholders do not gain any profit from the company but receive dividend payments.

2. What does non-participating liquidation preference mean?

The non participating liquidation preference of the preferred shareholders allows them to share in profits when the company is sold, but protects them from losses if the company exits at a lower value.

3. What is participating vs non-participating?

A participating policy makes the insured eligible to receive a share of the insurance company’s profits. These shares are called bonuses or dividends.

In non-participating policies, the profits are not shared and no dividends are paid to the policyholders.

4. What is a non-participating preference?

Preferred stocks are a type of security that pays a pre-determined amount of annual interest to their holders. This usually means that the holder of the stock must sign a document stating the minimum annual return they will receive.

5. What is the difference between participating and non participating preference shares in startup investing?

The difference between participating and non participating preference shares lies in how investors receive their returns during an exit. Participating preference shareholders receive their investment back first and then share in the remaining proceeds. Non-participating preference shareholders must choose between receiving their liquidation preference or converting their shares to participate in the proceeds.

6. Why do venture capitalists prefer participating liquidation preference?

Many venture capitalists prefer participating liquidation preferences because they provide downside protection while still allowing participation in the upside of successful exits. This structure helps improve portfolio returns, especially in moderate exit scenarios where returns might otherwise be limited.

Conclusion

When structuring an angel investment syndicate, it is important to understand the differences between participating vs non-participating liquidation preference. Participating liquidation preference allows investors to receive a return of their original capital plus a share of any remaining proceeds from the sale or exit of the company while non-participating liquidation preference does not allow for this additional return.

It is important to consider both types when structuring deals as they have different tax implications and can affect how much money each investor receives in case of a sale or exit.

For angel investors who are just beginning their venture investing journey, understanding these terms is critical. Concepts like liquidation preferences, ownership dilution, and exit distributions directly influence the financial outcomes of startup investments. By learning how these structures work in real-world deals, investors can evaluate opportunities more confidently and negotiate smarter investment terms.

This is exactly why many investors choose to deepen their knowledge through structured programs like Angel School’s Venture Fundamentals. The program helps aspiring angel investors understand deal structures, venture capital mechanics, and startup evaluation frameworks. By building a strong foundation in topics like participating vs non participating liquidation preference, investors can make more informed decisions and build a stronger, more resilient investment portfolio.

About AngelSchool.vc

AngelSchool.vc is the ultimate Accelerator for Angel Investors - from 1st check to leading syndicates as ‘Super Angels’. We give venture investors world-class training, a global community AND build their track record as a member of our Investment Committee (IC).

The AngelSchool.vc Syndicate is backed by 1500+ LPs and deploys $MNs annually. Subscribe here for exclusive dealflow.