This article is the 2nd in our 3-article series on SAFE conversions and dilution impacts.

The example provided shows the impact on ownership and dilution for both investors and Founders from 3 rounds of post-money SAFEs.

TLDR: Our key findings are:

- The shift from pre- to post-money SAFEs is largely favorable for investors; investors will simply be issued shares to maintain their post-money ownership stake.

- The dilution burden of multiple post-money SAFEs can be significant for Founders, especially when unplanned.

- Founders can mitigate this dilution risk through more diligent use of capital planning and operational execution at the pre-equity rounds.

In case you missed it, here’s the 1st article in this series where we examine pre-money SAFE conversion.

Introduction

Pre-money SAFEs were introduced by Y Combinator in 2013 and became a standard over convertibles for their simplicity.

This was updated to post-money conversion in 2018 and became broadly adopted in H2 2021. Our article ‘7 Ways post-money SAFES affect Founders and Angel Investors’ explains all these changes.

The most substantive impact of this change has to do with dilution. At the time of an equity qualified financing, SAFEs are converted:

- Pre-money SAFEs: Multiple rounds of post-money SAFES results in dilution for both by Founders and investors.

- Post-money SAFEs: Multiple rounds of post-money SAFES places dilution entirely on Founders.

Both pre-money and post-money SAFEs are subsequently diluted by the equity round.

The following example illustrates the impact on ownership and dilution for investors and Founders from 3 rounds of post-money SAFE financing. It simulates conversion during a qualified equity financing where the SAFEs convert at the valuation cap (not the discount).

Note that immediately following SAFE conversion, the equity financing results in new shares being issued which would introduce further dilution. This is not reflected in this calculation for simplicity.

Step 1: Company Founded

Upon founding the company, 100,000 shares are created and 10% is set aside for current and future employees. The founders retain 90,000 shares and allocate 10,000 to an ESOP.

Their cap table looks like this:

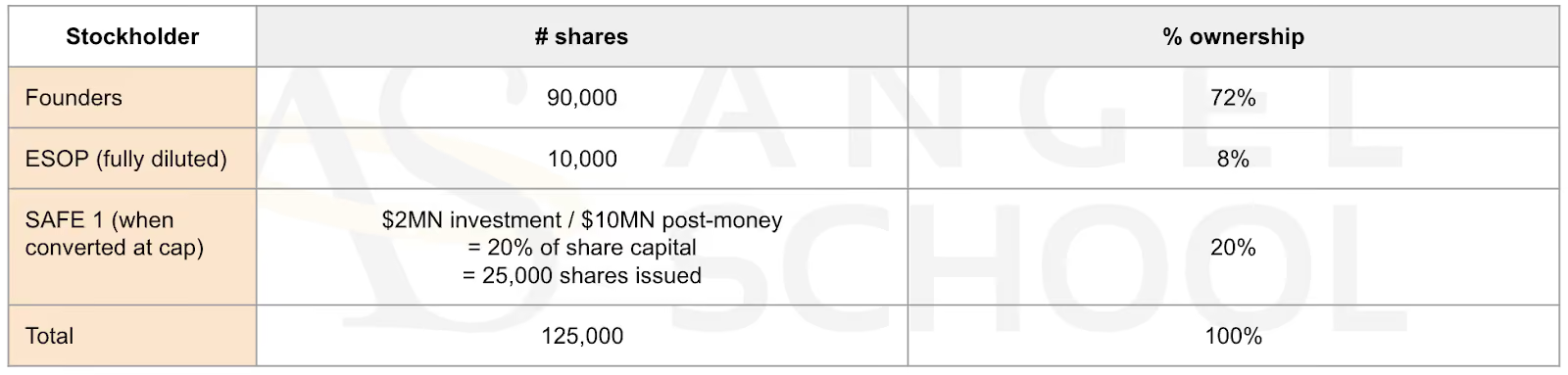

Step 2: Post-Money SAFE 1

The company raises $2MN on post-money SAFE. It has a valuation cap of $8MN pre ($10MN post) and 0% discount.

If an equity financing takes place above the $10MN valuation cap, the post-money SAFE converts to equity based on this calculation:

- SAFE 1 ownership = $2MN investment / $10MN post-money cap = 20% ownership

- 100,000 shares held by Founders and ESOP constitute 80%

- SAFE 1 therefore will be issued 20% / 80% x 100,000 = 25,000 shares

Prior to the equity round dilution, post-money SAFE 1 investors own 20% of the company. Founders and ESOP are diluted down to 72% and 8% respectively.

The resulting cap table looks like this:

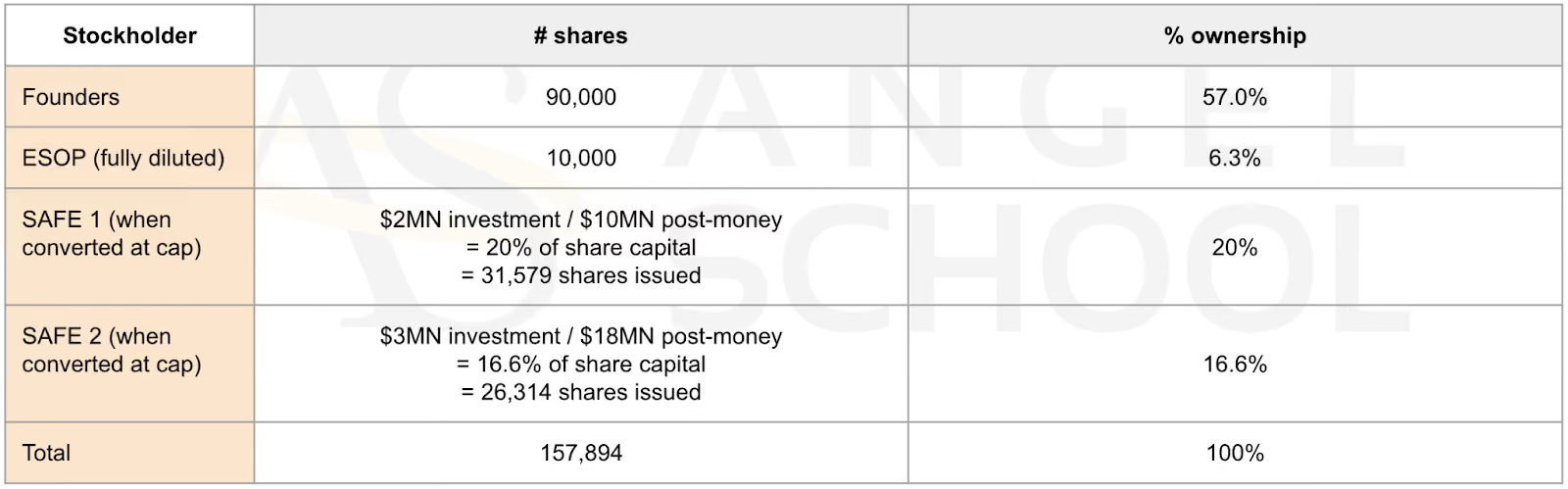

Step 3: post-money SAFE 2

Some time after taking in post-money SAFE 1, the company decides to raise an additional $3MN on a new post-money SAFE. It has a valuation cap of $15MN pre ($18MN post) and 0% discount.

If an equity financing takes place above the $18MN valuation cap, ownership will accrue as follows:

- SAFE 1 ownership = $2MN investment / $10MN post-money cap = 20% ownership

- SAFE 2 ownership = $3MN investment / $18MN post-money cap = 16.6% ownership

- 100,000 shares held by Founders and ESOP therefore constitute 63.3%

New shares will be issued as follows:

- SAFE 1 = 100,000 shares / 63.3% x 20% = 31,579 shares

- SAFE 2 = 100,000 shares / 63.3% x 16.6% = 26,314 shares

The resulting cap table looks like this:

Notice that the addition of SAFE 2 results in 57,894 new shares being created and issued to both SAFE 1 and SAFE 2 investors to maintain their respective 20% and 16.6% shares.

Founders now own 57% (down from 72% with only SAFE 1).

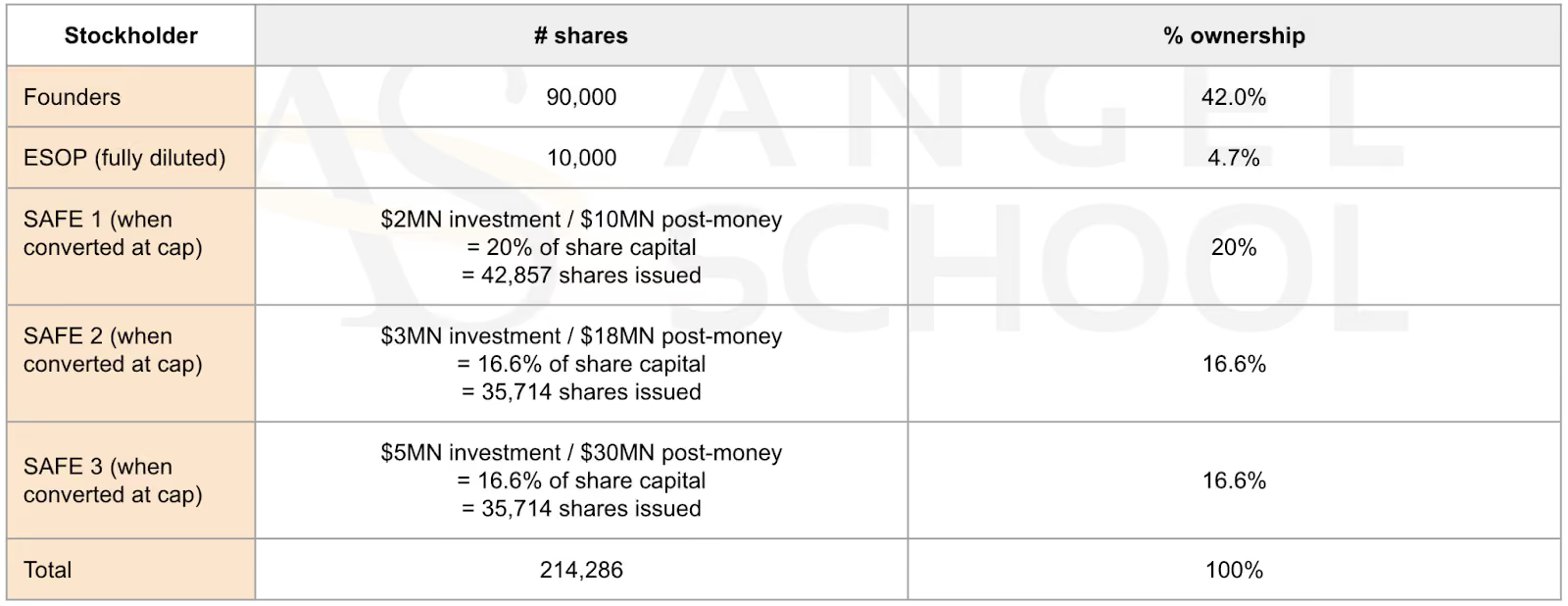

Step 4: post-money SAFE 3

Let’s say the company decides to take in additional SAFE financing. They raise an additional $5MN on a new post-money SAFE. It has a valuation cap of $25MN pre ($30MN post) and 0% discount.

If an equity financing takes place above the $30MN valuation cap, ownership will accrue as follows:

- SAFE 1 ownership = $2MN investment / $10MN post-money cap = 20% ownership

- SAFE 2 ownership = $3MN investment / $18MN post-money cap = 16.6% ownership

- SAFE 3 ownership = $5MN investment / $30MN post-money cap = 16.6% ownership

- 100,000 shares held by Founders and ESOP therefore constitute 46.7%

New shares will be issued as follows:

- SAFE 1 = 100,000 shares / 46.7% x 20% = 42,857 shares

- SAFE 2 = 100,000 shares / 46.7% x 16.6% = 35,714 shares

- SAFE 3 = 100,000 shares / 46.7% x 16.6% = 35,714 shares

The resulting cap table looks like this:

The addition of SAFE 3 results in 114,286 new shares being created and issued to SAFE 1, SAFE 2 and SAFE 3 investors to maintain their respective post-money ownership.

Founders now own 42% (down from 72% with only SAFE 1).

Conclusion

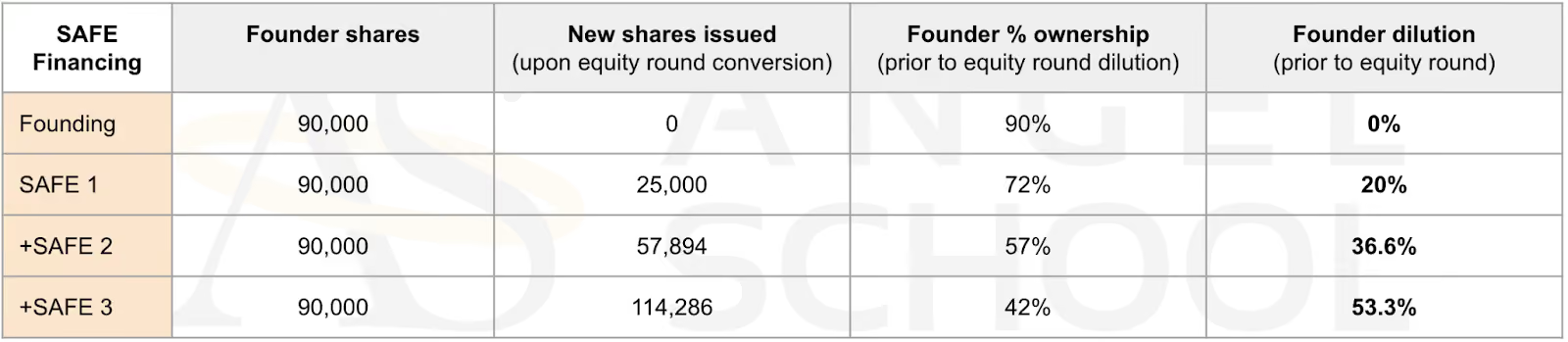

As an investor, the addition of new post-money SAFEs following your investment simply results in more shares being issued to you to maintain your ownership. The table below- based on our example- captures the dilution impact of post-money SAFEs 2 and 3 from the perspective of a SAFE 1 investor.

The dilution burden of multiple rounds of post-money SAFE financing solely impacts Founders upon conversion. The below table illustrates the dilution impact to Founders from our example.

Founders should focus on avoiding unplanned fundings, especially using post-money SAFEs. As such we recommend for Founders to pay particular attention to:

- Diligent forecasting of fundraising capital: Plan for what you need and fundraise accordingly.

- Operational execution and target setting: Model your business targets and track execution against it, especially where cashflow and runway may be impacted.

In case you missed it, here’s the 1st article in this series where we examine pre-money SAFE conversion.

About AngelSchool.vc

AngelSchool.vc is the ultimate Accelerator for Angel Investors - from 1st check to leading syndicates as ‘Super Angels’. We give venture investors world-class training, a global community AND build their track record as a member of our Investment Committee (IC).

The AngelSchool.vc Syndicate is backed by 1500+ LPs and deploys $MNs annually. Subscribe here for exclusive dealflow.